Original price was: KSh500.KSh399Current price is: KSh399.

Download Principles of Auditing April 2026 ATD Level III Answers

Description

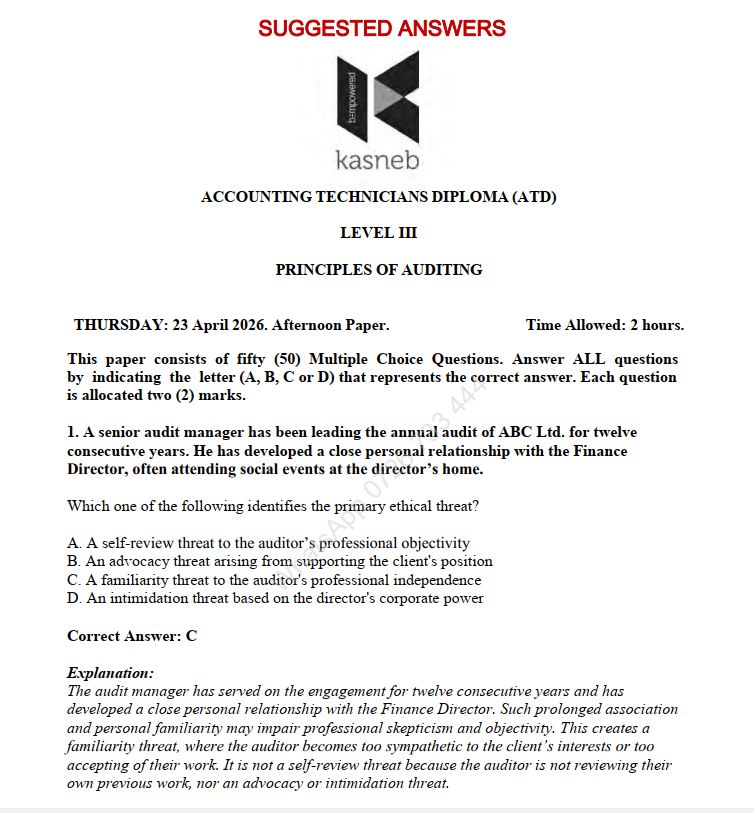

ACCOUNTING TECHNICIANS DIPLOMA (ATD) LEVEL III

Principles of Auditing ATD Level III Answers

THURSDAY: 23 April 2026. Afternoon Paper. Time Allowed: 2 hours.

This paper consists of fifty (50) Multiple Choice Questions. Answer ALL questions by indicating the letter (A, B, C or D) that represents the correct answer. Each question is allocated two (2) marks.

1. A senior audit manager has been leading the annual audit of ABC Ltd. for twelve consecutive years. He has developed a close personal relationship with the Finance Director, often attending social events at the director’s home.

Which one of the following identifies the primary ethical threat?

A. A self-review threat to the auditor’s professional objectivity

B. An advocacy threat arising from supporting the client’s position

C. A familiarity threat to the auditor’s professional independence

D. An intimidation threat based on the director’s corporate power (2 marks)

2. During the audit of PetTech, a software manufacturer, you discover that the senior accountant in charge of payroll colluded with the Chief Internal Auditor to override the internal control system.

This situation, where two or more people work together to avoid a control possibly for the purpose of committing fraud, illustrates .

A. a standard application control within the payroll system

B. an inherent limitation of an internal control system

C. a primary objective of the statutory audit engagement

D. the implementation of a reactive forensic audit procedure (2 marks)

3. While performing the annual audit of#8216;FTM Logistics’, the junior auditor is denied access to the minutes of the Board of Directors’ meetings. The Finance Director claims these documents are#8220;strictly confidential” and not for audit review.

Which one of the following statements BEST describes the auditor’s legal right in this scenario?

A. The auditor has no right to see documents marked as confidential

B. The auditor must obtain a court order to view any board minutes

C. The auditor has a statutory right of access to all books and records

D. The auditor can only see these minutes if the shareholders agree (2 marks)

4. Jitume Ltd. uses an automated sales system to process customer transactions. When a clerk enters a new order, the system automatically checks the customer’s current balance and rejects any order that exceeds the Sh.500,000 credit limit.

This specific IT control is an example of .

A. an application control over input validity and accuracy

B. a general IT control over data security and access logic

C. a physical control over the distribution of hardware

D. a performance review control over management budgets (2 marks)

5. While auditing trade receivables, an auditor identifies a balance for#8220;Jane Okoth” of Sh. 200,000, which is below the performance materiality of Sh.500,000. It is noted that Jane’s company has recently gone into liquidation.

The auditor should select this balance for testing because .

A. it represents a significant portion of current assets

B. it indicates a specific risk regarding debt valuation

C. the Companies Act requires testing all liquidated firms

D. it ensures the detection risk is reduced to zero levels (2 marks)

6. The registrar of companies has been informed that the current auditor of Omega Ltd. has been disqualified from practice. According to the legal framework, who has the power to appoint a successor to fill this casual vacancy before the next (Annual general Meeting (AGM)?

A. The board of directors of the company being audited

B. The shareholders must meet in a special session

C. The internal audit department takes over the duties

D. The previous auditor appoints his own replacement (2 marks)

7. Ufanisi operates a perpetual inventory system with rolling physical counts throughout the year, but they perform no year-end count. To verify the accuracy of the records, the auditor’s primary procedure is to .

A. recalculate the depreciation of the main warehouse

B. attend a selection of the rolling counts during the year

C. inquire of the warehouse manager about his tenure

D. vouch all sales invoices to the goods received notes (2 marks)

8. Many shareholders believe that an unmodified audit report provides a 100% guarantee that no fraud or error exists within the company’s records. This misunderstanding is an example of .

A. the agency theory relationship between directors and owners

B. professional skepticism required by international standards

C. a self-interest threat to the auditor’s professional integrity

D. the audit expectation gap between the public and auditors (2 marks)

9. A junior auditor is preparing the working paper files for a recurring client and needs to file the Articles of Association and long-term lease agreements.

Which one of the following statements is CORRECT regarding the location of these documents?

A. They should be kept in the current audit file only

B. They should be discarded after the engagement letter

C. They should be stored in the client’s internal safe

D. They should be kept in the permanent audit file (2 marks)

10. While performing analytical procedures, an auditor notes that revenue has decreased by 20%, but the total cost of sales has remained constant compared to the prior year.

Which one of the following actions is the auditor’s next logical step?

A. Issue a qualified audit opinion immediately for fraud

B. Investigate the gross profit margin further for errors

C. Ignore the discrepancy if it is less than total assets

D. Ask the directors to resign for poor stewardship (2 marks)

11. According to the provisions of ISA 210, which one of the following items is NOT a precondition for an audit that management must agree to before the engagement begins?

A. The use of an acceptable financial reporting framework

B. Management’s responsibility for the internal controls

C. Provision of unrestricted access to all audit evidence

D. The agreement to pay the audit fee within thirty days (2 marks)

12. The concept of stewardship in a limited liability company implies that the company’s directors are responsible for

.

A. personally, conducting the internal audit examinations.

B. safeguarding assets and managing them for shareholders

C. ensuring that the company never records a financial loss

D. appointing the external auditors at the end of the year (2 marks)

13. An auditor is testing the existence of motor vehicles recorded in the non-current asset register of a transport company. Which one of the following procedures would provide the MOST persuasive evidence for this assertion?

A. Vouching the purchase invoice to the cash book entry

B. Physical inspection of the vehicles and documents

C. Reviewing the board minutes for the purchase approval

D. Checking that the vehicles are in the asset register (2 marks)

14. During an audit, you find that the client’s inventory valuation is materially misstated. Management refuses to adjust the financial statements and you conclude the effect is material, but not pervasive. Which one of the following audit opinions should be expressed?

A. An unmodified opinion with an emphasis of matter

B. A qualified opinion using#8220;except for” phrasing

C. An adverse opinion stating accounts are not fair

D. A disclaimer of opinion due to lack of information (2 marks)

15. An assurance firm is considering using an independent specialist to value the client’s specialised machinery. Before relying on their work, the auditor should evaluate the specialist’s .

A. historical relationship with the company’s bankers

B. professional competence, capabilities and objectivity

C. internal training and development policy for staff

D. total number of employees and their marital status (2 marks)

16. A partner in an audit firm has been approached by a prospective client to perform the annual audit. Before accepting, the partner drafts a document to define the scope and responsibilities of the engagement. This document is known as the .

A. audit engagement letter for the incoming auditor

B. management representation letter for the period

C. internal control questionnaire for the sales team

D. audit programme for the specific year end work (2 marks)

17. According to International Standard on auditing (ISA) 580, an auditor obtains a specific document from management to confirm oral representations made during the audit and to support other audit evidence.

This document is known as .

A. letter of engagement detailing the audit scope

B. management representation letter for the auditor

C. internal control report for the board of directors

D. report to those charged with company governance (2 marks)

18. An auditor identifies that a client’s internal control system lacks proper segregation of duties because the same person who records cash receipts also performs the bank reconciliation. Which one of the following risks is most likely to be created?

A. A decrease in the auditor’s overall detection risk

B. The risk of misappropriation of cash being hidden

C. An increase in the company’s overall profitability

D. A reduction in the audit fee for the coming year (2 marks)

19. A shareholder at an Annual General Meeting (AGM) argues that the auditor is negligent because they did not find a minor clerical error in the petty cash records. Which one of the following statements BEST clarifies the auditor’s responsibility?

A. The auditor is responsible for detecting all errors, regardless of size

B. The auditor’s focus is on material misstatements in the financial reports

C. The auditor must check every single transaction within the petty cash

D. The auditor is an insurer of the company’s future financial performance (2 marks)

20. When an auditor is performing a#8220;Walk-through Test” on the sales system of a large wholesaler, his primary objective is to .

A. count all the petty cash takings in the office safe

B. confirm his understanding of the internal controls

C. issue a certificate of accuracy to the shareholders

D. negotiate the final amount for the audit fee (2 marks)

21. During the audit of a public limited company, the engagement team is reviewing the auditor’s duties as defined by the Companies Act. Which one of the following is regarded as the auditor’s primary duty?

A. To detect all instances of fraud and minor error

B. To prepare the company’s annual financial statements

C. To express an opinion on the fairness of the accounts

D. To manage the company’s internal control environment (2 marks)

22. While observing a client’s annual physical inventory count, an auditor noticed that certain test counts were higher than the recorded quantities in the client’s records. This situation could result from the client’s failure to record

.

A. sales that occurred before the count date

B. purchase discounts offered by the suppliers

C. purchase returns that were sent to vendors

D. sales returns that were received from customers (2 marks)

23. An auditor finds that a company is experiencing severe cash flow difficulties and is unable to pay its trade creditors on time. The auditor’s primary concern in this scenario relates to .

A. the adequacy of general IT controls and security

B. the valuation of all non-current tangible assets

C. the use of the going concern basis for the period

D. the appointment of the internal audit committee (2 marks)

24. A retail company’s internal control system requires that all sales over Sh.100,000 must be authorised by the store manager. If the auditor finds that multiple sales of Sh.120,000 were processed without this signature, it indicates a

.

A. failure in the operating effectiveness of controls

B. high inherent risk within the entire retail sector

C. lack of professional scepticism by the manager

D. misunderstanding of the audit expectation gap (2 marks)

25. An auditor is reviewing the physical controls over the high-value inventory of a jewellery wholesaler. Which one of the following internal control activities would be the MOST effective at preventing the unauthorised removal of stock from the premises?

A. Reconciling the monthly sales day book to the general ledger

B. Requiring two staff members to sign for all inventory movements

C. Maintaining an un-numbered list of all staff personal contacts

D. Ensuring that all accounting software uses a standard password (2 marks)

26. A member of the public believes that an auditor’s unmodified report on the financial statements of#8216;Delta Logistics’ serves as a guarantee that the company is 100% free from all errors and will remain profitable for the foreseeable future. Which one of the following auditing concepts BEST describes this common misunderstanding?

A. The principle of professional skepticism

B. The concept of the audit expectation gap

C. The statutory right of access to records

D. The fundamental principle of objectivity (2 marks)

27. An auditor is concerned that trade payables may be understated because the client has not recorded all invoices received. To test the completeness of payables, the auditor should .

A. reconcile supplier statements to the ledger accounts

B. vouch ledger entries to the supporting invoices

C. confirm the existence of the recorded balances

D. recalculate the depreciation on non-current assets (2 marks)

28. A retail company uses an automated accounting system to process its sales. To ensure only valid transactions are entered, the system requires a unique employee identification number and password. This is a(n)

.

A. general IT control over access to programs and data

B. application control over input completeness

C. hardware control over processing speed

D. output control over data distribution (2 marks)

29. During the course of the audit, the shareholders of Beta Ltd. wish to remove the auditor from office before his term expires. According to the law, which mechanism must be used to achieve this?

A. A board of directors’ executive decision

B. A special notice and an ordinary resolution

C. A petition to the Registrar of Companies

D. An ordinary resolution at a special meeting (2 marks)

30. An audit firm has found that their appointment as auditors for a new client was not handled according to statutory procedures. Which one of the following bodies is responsible for the regulation and licensing of auditors to ensure such standards are met?

A. The Registrar of Companies for the jurisdiction

B. The Professional Accountancy Organisation (PAO)

C. The Internal Audit Foundation of the company

D. The Board of Directors of the specific entity (2 marks)

31. An audit firm accepts an engagement for a fee that is significantly lower than the fee charged by the previous firm. This practice, known as#8220;low-balling”, creates a potential threat to .

A. professional behaviour and client confidentiality

B. professional competence and due professional care

C. objectivity arising from the self-interest threat

D. integrity due to the advocacy threat created (2 marks)

32. What should an auditor do if a prospective new audit client refuses to allow him to communicate with the existing auditor regarding the client’s business affairs?

A. Contact the existing auditor without permission

B. Refuse to take on the new audit client

C. Contact the client’s legal counsel for advice

D. Accept the client but increase the audit fee (2 marks)

33. When an organisation adopts new technologies such as cloud computing and blockchain, the internal audit function must be reoriented. This reorientation is necessary to ensure .

A. the auditor can replace all substantive testing

B. all manual files are converted to digital form

C. audit strategies suit the digital environment

D. the audit fee is reduced by at least fifty percent (2 marks)

34. In an e-commerce business, a control designed to ensure that a customer cannot submit an order without entering a valid delivery address is best described as a(n) .

A. hash total check

B. range check limit

C. on-screen prompt

D. sequence check (2 marks)

35. To ensure that the figure for total sales recorded in the general ledger is complete, an auditor should perform which one of the following procedures?

A. Vouch entries from the sales ledger to invoices

B. Compare the sales budget to the actual results

C. Trace goods dispatch notes to the sales invoices

D. Recalculate the mathematical accuracy of invoices (2 marks)

36. An auditor is designing an external confirmation request for trade receivables. Which one of the following factors would MOST significantly increase the reliability of the evidence obtained?

A. Sending the requests via the client’s internal mail

B. Using a negative confirmation for material balances

C. Requesting the client’s staff to follow up on non-replies

D. Having the responses sent directly to the auditor (2 marks)

37. Audit documentation is the property of the auditor and must be kept confidential. Which one of the following items is a primary reason for preparing this documentation?

A. To provide a basis for the next year’s audit fee

B. To replace the company’s official accounting books

C. To support the auditor’s conclusion and opinion

D. To list the performance reviews of the client’s staff (2 marks)

38. In the context of audit sampling,#8220;sampling risk” is best defined as the risk that .

A. the sample chosen is not representative of the population.

B. the auditor’s procedures will fail to detect every fraud.

C. the auditor uses an inappropriate testing procedure.

D. the sample size is too small to be mathematically valid. (2 marks)

39. In an IT-based accounting system, a control that requires a user to input a specific password before they can access or change the payroll master file is a(n) .

A. sequence check

B. batch total sum

C. field check limit

D. access control (2 marks)

40. An auditor’s report expresses an opinion on whether the financial statements give a#8220;true and fair view.” This concept implies that the financial statements .

A. are factual, impartial, and free from material error

B. contain zero errors and are 100% mathematically accurate

C. were prepared by the auditor on behalf of management

D. comply with the personal beliefs of the company directors (2 marks)

41. During the audit of Alpha Exports, the engagement team discovers possible non-compliance with international trade laws that could result in material fines and disclosure in the financial statements. If management and those charged with governance do not take appropriate action, which one of the following is the MOST appropriate response by the auditor?

A. Assess the effect on the financial statements and consider the impact on the auditor’s report

B. Disregard the matter and proceed with the audit after documenting management’s explanation

C. Suspend the engagement and require management to correct the non-compliance before completion

D. Report the matter to the Registrar immediately and then issue the audit report without change (2 marks)

42. An auditor uses#8220;Directional Testing” to detect the potential understatement of trade payables. Which one of the following is the correct starting point for this test?

A. The balances recorded in the primary purchase ledger

B. The total profit shown in the statement of income

C. The bank confirmation letter from the central bank

D. Reciprocal populations such as goods received notes (2 marks)

43.#8220;Professional Skepticism” is a fundamental concept in auditing which requires the auditor to .

A. assume that the client’s management is always dishonest.

B. disregard any audit evidence provided by the client’s staff

C. maintain a questioning mind and critically assess evidence

D. only accept evidence that is obtained from external sources (2 marks)

44. Which one of the following identifies a fundamental principle of the professional code of ethics that requires an auditor to be straightforward and honest in all business relationships?

A. Objectivity

B. Confidentiality

C. Integrity

D. Competence (2 marks)

45. While finalising the audit file for#8216;Modern Paints Ltd’, the senior auditor ensures that all working papers clearly state the objective of the test, the work performed, and the conclusion reached. What is the PRIMARY purpose of this detailed documentation?

A. To allow the client’s staff to see the audit strategy

B. To serve as a basis for calculating the final audit fee

C. To support the conclusion and the audit opinion issued

D. To replace the need for an external quality control review (2 marks)

46. When there is a material disagreement between the auditor and management regarding an accounting policy, and the effect is NOT pervasive, the auditor should issue a(n) .

A. adverse opinion

B. unmodified opinion

C. qualified opinion

D. disclaimer of opinion (2 marks)

47. An auditor is currently in the process of deciding the nature, timing, and extent of the audit procedures to be performed for a new client. This stage of the audit is best described as .

A. audit reporting

B. audit planning

C. audit completion

D. audit evidence (2 marks)

48. Which one of the following ethical principles requires an auditor to not allow bias or conflict of interest to override professional judgments?

A. Objectivity

B. Integrity

C. Confidentiality

D. Professional competence (2 marks)

49. An auditor’s independence may be threatened if the audit fees from one client represent a very large proportion of the firm’s total income. This is a(n) .

A. advocacy threat

B. familiarity threat

C. self-interest threat

D. self-review threat (2 marks)

50. In which one of the following situations MUST a resigning auditor deliver a written statement of circumstances to the company’s registered office?

A. Only if the auditor is removed by the board

B. If the auditor has found a minor clerical error

C. Only if the audit fee has not been paid in full

D. If there are matters that should be told to members (2 marks)

………………………………………………………………………………