Original price was: KSh500.KSh499Current price is: KSh499.

Download Principles of Taxation December 2025 ATD Level II Answers

Description

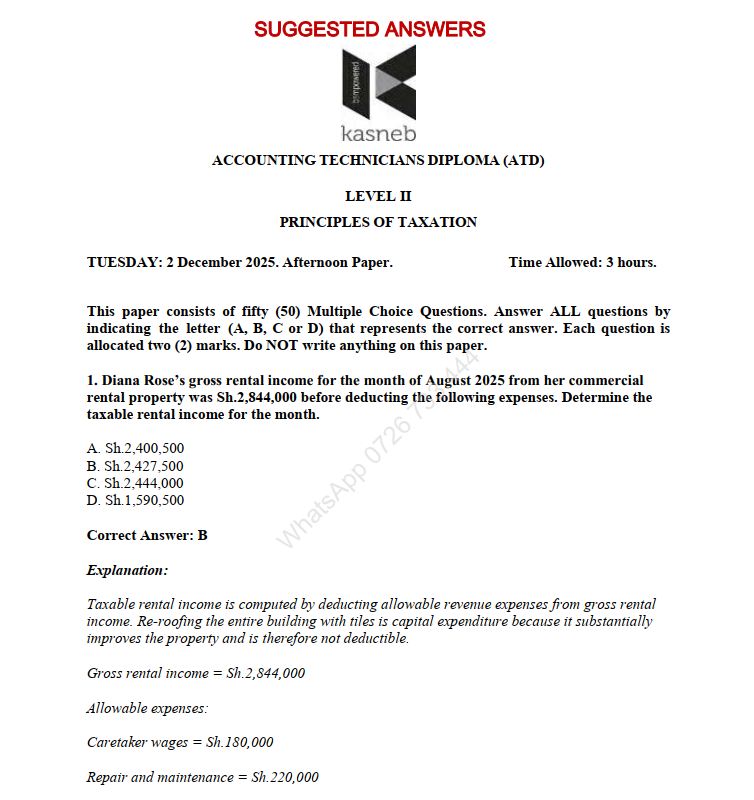

ACCOUNTING TECHNICIANS DIPLOMA (ATD) LEVEL II

PRINCIPLES OF TAXATION

TUESDAY: 2 December 2025. Afternoon Paper. Time Allowed: 3 hours.

This paper consists of fifty (50) Multiple Choice Questions. Answer ALL questions by indicating the letter (A, B, C or D) that represents the correct answer. Each question is allocated two (2) marks. Do NOT write anything on this paper.

1. Diana Rose’s gross rental income for the month of August 2025 from her commercial rental property was Sh.2,844,000 before deducting the following expenses:

Sh.

Caretaker wages 180,000

Re-roofing the entire building with tiles 810,000

Repair and maintenance 220,000

Mortgage interest 27,000

Water and electricity 16,500

Required:

Determine the taxable rental income for Diana Rose for the month of August 2025.

A. Sh.2,400,500

B. Sh.2,427,500

C. Sh.2,444,000

D. Sh.1,590,500 (2 marks)

2. Which one of the following conditions is CORRECT with respect to medical benefit?

A. It is a tax-free benefit to employee provided the employee is employed on a permanent basis

B. It is a tax-free benefit to employee provided the employee contributes to the scheme

C. It is a taxable benefit if only employer contributes to the scheme

D. It is a tax-free benefit provided the scheme is not discriminatory (2 marks)

3. Which one of the following statements is NOT a positive role of excise duty in an economy?

A. It protects local industries from cheap imports

B. It raises revenue for the government

C. It discourages consumption of harmful products

D. It discourages growth of local industries (2 marks)

4. Larry Mwendwa is an employee of Braze Ltd. During the year 2025, he reported an income of Sh.1,550,000 before housing benefits. He was housed in a fully furnished house. The cost of the furniture to the employer was Sh.124,000. The employer had rented the house from a related party where he paid Sh.35,000 per month while the market rental value of the house was Sh.40,000.

Determine Larry Mwendwa’s taxable income for the year ended 31 December 2025.

A. Sh.1,799,612

B. Sh.1,984,880

C. Sh.2,044,880

D. Sh.2,289,618 (2 marks)

5. The following instruments are not chargeable to stamp duty, EXCEPT .

A. instrument of divorce

B. letter of allotment of shares

C. mortgage agreements

D. acknowledgement of debt (2 marks)

6. Which one of the following measures CANNOT be used by the customs and excise duty departments of your country to prevent dumping?

A. Establishment of the advisory committee to recommend to the minister the imposition of antidumping or countervailing measures on investigated products imported into the country

B. Prohibition and restriction of all imports as per the law in force from time to time

C. Pre-shipment and pre-verification of exports done by qualified and reputable inspection firms and institutions of regular off-shore inspections

D. Collusion between customs officers and importers are policed strictly and heavily penalised (2 marks)

7. Which one of the following strategies CANNOT be used by a Revenue Authority to enhance tax compliance?

A. Creating awareness by the revenue authority on the roles of taxes and the civic duty to pay taxes

B. Increasing the rates of various taxes for example customs duty and value added tax (VAT)

C. Enhancing efficiency in tax collection for example requiring PIN in some transactions

D. Providing more tax incentives for example tax reliefs and allowances (2 marks)

8. Which one of the following assessments is NOT a binding assessment that is final and conclusive?

A. Assessment determined by local committee

B. Assessment made and no appeal has been made

C. Assessment made and no objection has been raised within the statutory period

D. Assessment awaiting determination by local committee (2 marks)

9. The following are circumstances under which a late objection could be accepted by the commissioner, EXCEPT

.

A. When the tax payer has no power in the office

B. When the tax payer is sick to the extent that he/she cannot handle his/her tax matters

C. When the tax payer was out of the country

D. When the tax payer is held in a police custody (2 marks)

10. The revenue authority could take the following actions to recover overdue tax, EXCEPT .

A. Holding property of the tax payer as security for the unpaid tax

B. Ask the bank to freeze the bank accounts of defaulters

C. Issue of distrait order where the assets of the tax payer are auctioned to recover the tax due and payable

D. The commissioner can prosecute the tax payer for the tax due and payable (2 marks)

11. The following are benefits of integrating functions of various departments of the revenue authority, EXCEPT

.

A. it enhances efficiency

B. it reduces operational costs

C. it reduces tax collected

D. it increases customer satisfaction (2 marks)

12. Edna Mulya is an employee of Base Ltd. During the year ended 31 December 2024, she contributed Sh.6,000 per month to Uzima insurance for her personal life insurance premium. How much was her insurance relief for the year?

A. Sh.21,600

B. Sh.10,800

C. Sh.10,000

D. Sh.21,000 (2 marks)

13. The following documents should accompany a self-assessment return to the revenue authority, EXCEPT

.

A. a list of customers and suppliers

B. a set of final accounts fully audited

C. tax computation schedule

D. documents supporting instalment tax paid (2 marks)

14. Tembo Ltd. sold goods to Laly Ltd., a withholding tax agent, in October 2025 for Sh.999,050 inclusive of 16% value added tax (VAT). What is the amount of VAT paid by Tembo Ltd. on the due date in regard to the goods?

A. Sh.159,848

B. Sh.137,800

C. Sh.120,575

D. Sh.17,225 (2 marks)

15. The following circumstances could lead to import duty paid be refunded, EXCEPT .

A. where it was paid in error as a result of wrong calculation or overpayment

B. where the imported goods are returned to the seller

C. where goods are used to manufacture for local consumption

D. where goods are destroyed or damaged while under custom control (2 marks)

16. Which one of the following statements is NOT a challenge associated with harmonisation of taxation policies across East Africa region?

A. Member countries have the same tax laws

B. Difference in level of technology development

C. Political environment and good will of member states

D. Lack of competent personnel (2 marks)

17. Smart Manufacturing Ltd. started operations on 1 January 2024. In the month of September 2024, the company imported a processing machine for Sh.1,800,000 being cost. The insurance company charged 4% of the value of the machine and cargo handling company charged 3% of the value being freight charges. Import duty rate was 25% during the month while VAT rate was 16%. What is the qualifying cost for investment allowance which could be claimed by Smart Manufacturing Ltd. in respect of processing machine?

A. Sh.2,610,000

B. Sh.2,792,700

C. Sh.2,407,500

D. Sh.2,714,400 (2 marks)

18. Seaway Ltd. started operations in the year 2024 after incurring various capital expenditures among them a ship at a cost of Sh.324,000,000, computers Sh.180,000 and a weighing scale Sh.98,000. What is Seaway Ltd.’s investment allowance for the year 2024?

A. Sh.324,000,000

B. Sh.165,203,000

C. Sh.162,139,000

D. Sh.162,054,800 (2 marks)

19. Esther Atoni received a basic salary of Sh.1,359,600 in year 2024. She also received an annual medical allowance of Sh.400,000 which was available to senior staff only. The company paid Sh.150,500 to a school where her child attends. The amount paid for the school fees was not debited in the books of the company. What is Esther Atoni’s taxable income for the year 2024?

A. Sh.1,709,600

B. Sh.1,510,100

C. Sh.1,910,100

D. Sh.1,759,600 (2 marks)

20. Pangani Ltd. is a manufacturing company that prepares its accounts on 31 December every year. On 1 February 2024, the company imported a processing machinery and incurred the following costs:

• Cost of machinery

• Freight charges

• Insurance on transit

• Duty paid

• Installation costs

Required:

What is the qualifying cost of investment allowance which can be claimed by Pangani Ltd. in respect of the processing machinery?

A. Sh.975,000

B. Sh.1,005,000

C. Sh.1,170,000

D. Sh.1,335,000 (2 marks)

21. Getway Ltd. reported a net taxable profit of Sh.14,040,000 for the year ended 31 December 2024. The instalment tax paid during the year ended 31 December 2024 was Sh.3,729,000.

Required:

Determine the net tax payable (if any) by Getway Ltd. for the year ended 31 December 2024.

A. Sh.212,000

B. Sh.483,000

C. Sh.263,600

D. Sh.118,700 (2 marks)

22. Fuata Limited started operations during the year 2024 after incurring various capital expenditures among them a saloon car which was purchased at a cost of Sh.3,250,000 and computers at a cost of Sh.1,800,000. Determine the wear and tear deduction for tax purposes for the company for the year ended 31 December 2024.

A. Sh.1,515,000

B. Sh.960,000

C. Sh.1,150,000

D. Sh.1,200,000 (2 marks)

23. Patts Manufacturers Ltd. commenced its operations on 1 January 2024 after incurring the following expenditure:

Sh.

• Factory building 15,480,000

• Plant and machinery 2,250,000

• Saloon car 3,200,000

• Mobile forklift 1,100,000

• Generator 960,000

The cost of the building includes cost of land Sh.1,250,000 and sports pavilion Sh.600,000.

Required:

Determine the investment allowance due to Patts Manufacturers Ltd. for the year 2024.

A. Sh.9,121,000

B. Sh.9,986,000

C. Sh.9,505,000

D. Sh.9,445,000 (2 marks)

24. Which one of the following is NOT a drawback of capital allowances?

A. It is enjoyed mostly by manufacturers, thereby, discriminating other economic players

B. It is enjoyed mostly by the poor, thereby, reducing the gap between the rich and the poor

C. Investors close shop and move to other destinations once the tax incentive cease

D. It results in loss of revenue for the government as it reduces tax payable (2 marks)

25. The following are circumstances under which a taxpayer may be exempted from paying instalment tax, EXCEPT

.

A. total tax payable in any year of income exceeds Sh.40,000

B. income other than employment income is less than one third of total income

C. if tax payer’s total tax liability for that year of income is nil to the best of their judgement

D. individual’s only source of income is employment and all taxes have been paid in full through PAYE tax

(2 marks)

26. The following arguments are in favour of introduction of capital gains tax (CGT) in an economy, EXCEPT

.

A. it ensures that there is equity in taxation

B. it helps in curbing inflation

C. it increases chances of tax avoidance

D. it increases government revenue (2 marks)

27. Which one of the following statements explains the meaning of advance tax?

A. Tax levied on commercial vehicles before being licensed to operate in Kenya

B. Tax levied by the government for certain transactions and documents

C. Tax levied on locally manufactured goods

D. Tax levied on incomes earned by an individual (2 marks)

28. Ladah Ltd. reported a net loss of Sh.441,000 for the year ended 31 December 2024 after deducting the following expenses:

Sh.

Cash embezzled by cashier 274,000

Legal fees 222,000

Allowance for doubtful debt 404,000

License and permits 317,000

Salaries and wages 561,000

Goodwill amortised 411,000

Required:

Determine the adjusted taxable profit (loss) for Ladah Ltd.

A. Sh.935,000

B. Sh.1,119,000

C. Sh.648,000

D. Sh.1,530,000 (2 marks)

29. Bidii Ltd. sold goods to Camila Ltd. worth Sh.699,886 inclusive of VAT and exported goods to Zana Ltd., a company based in Tanzania, for Sh.725,500 in December 2024. The rate of VAT applicable in the month was 16%. What is the value of VAT payable in relation to these transactions?

A. Sh.116,080

B. Sh.96,536

C. Sh.212,616

D. Sh.196,604 (2 marks)

30. Zakozi Ltd. sold goods to Adimo Ltd., a withholding tax agent, for Sh.606,216 inclusive of 16% value added tax. What is the amount of VAT paid by Zakozi Ltd on the due date in regards to the goods sold?

A. Sh.83,616

B. Sh.10,452

C. Sh.78,390

D. Sh.73,164 (2 marks)

31. Martha Ndiana is an employee of Nero Ltd. During the year ended 31 December 2024, her computed pay as you earn (PAYE) before deducting personal relief and insurance relief was Sh.216,800. She contributed Sh.9,000 per month to Maisha insurance for her personal life insurance premium. Determine her net PAYE for the year.

A. Sh.188,000

B. Sh.171,800

C. Sh.216,000

D. Sh.200,600 (2 marks)

32. Fubara Ltd. had the following expenses in their financial statement for the year ended 31 December 2024:

Sh.

• Advertisement 387,450

• Depreciation 279,300

• Subscription to chamber of commerce 372,750

• Goodwill amortisation 418,950

• Directors christmas party 483,000

• Bad debts written off 241,500

Required:

Determine the total non-allowable expense for Fubara Ltd. for income tax purposes.

A. Sh.698,250

B. Sh.1,181,250

C. Sh.1,085,700

D. Sh.1,117,200 (2 marks)

33. Clayman Ltd. sold goods to Elite Ltd., a withholding tax agent, in August 2025 for goods valued at Sh.720,000 exclusive of VAT. The applicable VAT rate was 16%. What is the amount of VAT paid by Clayman Ltd. on the due date in regard to the goods sold?

A. Sh.86,897

B. Sh.115,200

C. Sh.100,800

D. Sh.14,400 (2 marks)

34. The following circumstances can lead a government to revoke the licence of a manufacturer of excisable goods, EXCEPT .

A. the licensee has been convicted of an offence involving dishonesty or fraud

B. the licensee is guilty of an offence under the custom and excise duty

C. if the licensee has become bankrupt

D. if the licensee borrows operational funds outside the country (2 marks)

35. Which one of the following conditions is NOT a requirement for a valid memorandum of appeal?

A. It must be made in writing

B. It must state the ground of appeal in clear and concise manner

C. It must be signed by the commissioner

D. It must be accompanied with statement of fact with copies and original (2 marks)

36. Lilian Ekuna was employed as a casual cook by Rembe Ltd. for four weeks only in the month of December 2024. Each week she earned Sh.5,000. Determine her tax liability at the end of the month of December 2024.

A. Sh.2,000

B. Nil

C. Sh.2,400

D. Sh.4,800 (2 marks)

37. Essy Mulei operates an executive salon business. She has reported a net profit of Sh.3,375,000 for the year ended December 2024 after deducting the following expenses:

Sh.

Salaries and wages to workers 750,000

Licenses and permits 36,000

Rent 450,000

Detergents and perfumes 315,000

Water bills 125,000

Purchase of dryer 900,000

Maintenance of machines 150,000 Electricity prepaid at the end of the year 39,000 Depreciation 93,750

Subscriptions to saloon owners’ association 187,500 Wear and tear approved by revenue authority 117,800

Required:

Compute Essy Mulei’s taxable income.

A. Sh.4,368,750

B. Sh.4,314,000

C. Sh.4,407,750

D. Sh.4,617,000 (2 marks)

38. Which one of the following is NOT a non-taxable benefit from employment?

A. Employer’s contribution on behalf of the employee to a registered pension scheme

B. Employer’s contribution on behalf the employee to life insurance policy

C. Employee benefiting from employer’s non-discriminatory medical scheme

D. School fees paid by the employer for the employee’s children if it was taxed on the employer (2 marks)

39. Speedway Ltd. started operations in year 2024 after incurring various capital expenditures among them a saloon car which was purchased at a cost of Sh.3,800,000 and a delivery van at a cost of Sh.2,400,000. What was the company wear and tear deduction for tax purposes for the year 2024?

A. Sh.1,550,000

B. Sh.1010,000

C. Sh.1,262,500

D. Sh.1,350,000 (2 marks)

40. Skika Telecoms started its operations on 1 January 2024 after acquiring telecommunication equipment for Sh.1,920,000, computers worth Sh.360,000 and other machines worth Sh.480,000. Determine the investment allowance claimable by the company for the year ended 31 December 2024.

A. Sh.282,000

B. Sh.330,000

C. Sh.240,000

D. Sh.276,000 (2 marks)

41. Which one of the following statements clearly explains the difference between “tax evasion” and “tax avoidance”?

A. Both tax evasion and tax avoidance are illegal, but tax evasion involves providing the revenue authority with deliberately false information

B. Tax evasion is illegal, whereas tax avoidance involves the minimisation of tax liabilities using any lawful means

C. Both tax evasion and tax avoidance are illegal, but tax avoidance involves providing the revenue authority with deliberately false information

D. Tax avoidance is illegal, whereas tax evasion involves the minimisation of tax liabilities using any lawful means (2 marks)

42. Mashua Ferry Ltd. started shipping operations in the year 2024 after incurring various capital expenditures among them a ship of 220 tonnes which was purchased at a cost of Sh.20,400,000. What is Mashua Ferry Ltd.’s investment allowance for the year 2024?

A. Sh.10,200,000

B. Sh.5,100,000

C. Sh.204,000

D. Sh.20,400,000 (2 marks)

43. The following are circumstances under which the income of a married woman could be taxed at arm’s length, EXCEPT .

A. if they are separated and the separation is likely to be permanent

B. they are separated through a competent court jurisdiction

C. she is an employee of a trust or settlement created by the father

D. she is a resident and the husband is not (2 marks)

44. The following documents should accompany claim of refund for bad debts, EXCEPT .

A. confirmation from liquidator that debtors has become insolvent and proof of debts amount

B. copies of relevant tax invoices issued at time of supply to the insolvent debtors

C. a declaration that the debtor and the tax payer are related

D. records or documents showing input tax paid by the tax payer (2 marks)

45. Timothy Boi obtained a loan amounting to Sh.5,400,000 from his employer, Asam Ltd., at an interest rate of 9% per annum while the market rate was 12% per annum. What is the fringe benefit tax per month?

A. Sh.4,725

B. Sh.3,375

C. Sh.4,050

D. Sh.2,700 (2 marks)

46. Oprah Manga is an employee of Weru Ltd. During the year ended 31 December 2024, she was provided with a pick-up 2500cc which had cost the company Sh.2,400,000 in the year 2023. How much was the car benefit due to Oprah Manga for the year ended 31 December 2024?

A. Sh.576,000

B. Sh.600,000

C. Sh.720,000

D. Sh.288,000 (2 marks)

47. Tamara Ltd. started its mining operations on 1 January 2024 after acquiring mining machinery for Sh.12,000,000 and other machines worth Sh.332,000. Determine the investment allowance claimable by the company for the year ended 31 December 2024.

A. Sh.6,000,000

B. Sh.6,166,000

C. Sh.6,033,200

D. Sh.1,233,000 (2 marks)

48. Sonnie Chebaibai received a basic salary of Sh.1,236,000 during the year 2024. She also received an annual medical allowance of Sh.225,000 which was available to senior staff only. The company paid Sh.187,500 as school fee for her child direct to the school account. The amount paid for the school fees was debited in the company books of account. What is Sonnie Chebaibai’s taxable income for the year 2024?

A. Sh.1,461,000

B. Sh.1,423,500

C. Sh.1,400,500

D. Sh.1,648,500 (2 marks)

49. Which one of the following statements explains the earliest when value added tax (VAT) is due and payable?

A. When an invoice is issued in respect of supply

B. When the goods are manufactured and packed for distribution

C. When a quotation is requested

D. When an order is raised (2 marks)

50. Which one of the following incomes for savings and credit co-operative societies (SACCOs) is exempted from taxation?

A. Rental income

B. Interest from member loans

C. Interest income

D. Dividend income (2 marks)

………………………………………………………………………