Original price was: KSh500.KSh399Current price is: KSh399.

Download Principles of Auditing December 2025 ATD Level III Answers

Description

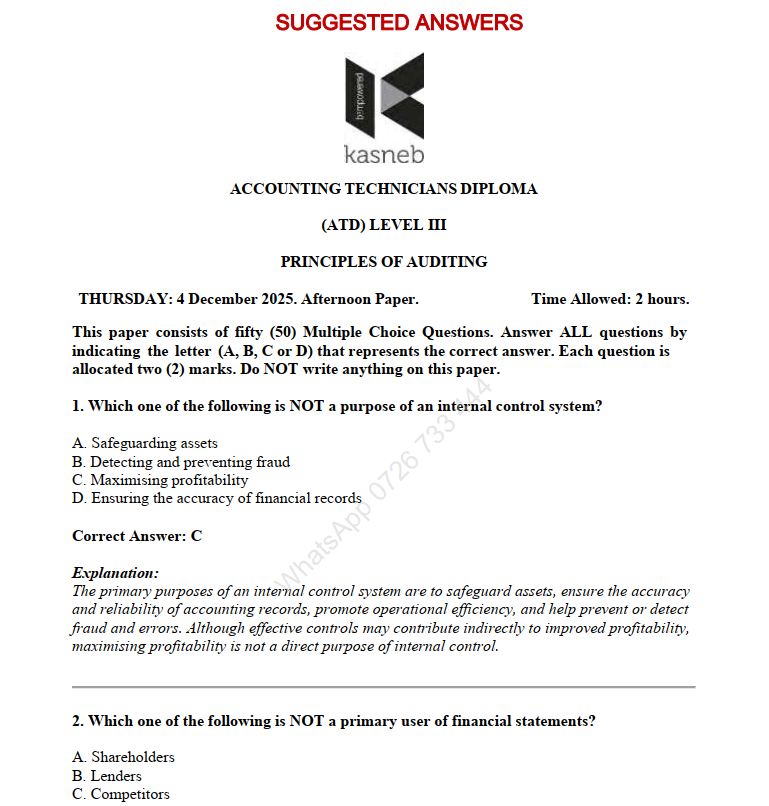

ACCOUNTING TECHNICIANS DIPLOMA (ATD) LEVEL III

PRINCIPLES OF AUDITING

THURSDAY: 4 December 2025. Afternoon Paper. Time Allowed: 2 hours.

This paper consists of fifty (50) Multiple Choice Questions. Answer ALL questions by indicating the letter (A, B, C or D) that represents the correct answer. Each question is allocated two (2) marks. Do NOT write anything on this paper.

1. Which one of the following is NOT a purpose of an internal control system.

A. Safeguarding assets

B. Detecting and preventing fraud

C. Maximising profitability

D. Ensuring the accuracy of financial records (2 marks)

2. Which one of the following is NOT a primary user of financial statements?

A. Shareholders

B. Lenders

C. Competitors

D. Auditors (2 marks)

3. The objective of tests of details of classes of transactions performed as substantive test is to .

A. comply with international financial reporting standards (IFRS)

B. attain assurance about the reliability of the information system

C. detect material misstatement at the assertion level

D. evaluate whether management’s controls operated effectively (2 marks)

4. The following are benefits of adequate audit planning, EXCEPT .

A. ensures sufficient attention is given to high-risk areas

B. helps auditors identify and resolve problems timely

C. eliminates the need for reliance on internal controls

D. assists in directing and supervision of team members (2 marks)

5. Analytical procedures during audit planning are performed mainly to .

A. detect fraud in the financial statements

B. understand the client’s business and operations

C. set audit fees

D. test internal controls (2 marks)

6. When evaluating internal controls, the auditor’s main objective is to .

A. guarantee the accuracy of the accounting records

B. eliminate the need for substantive testing

C. determine the degree of reliance to place on the accounting records

D. detect all errors and frauds in the accounting system (2 marks)

7. Which one of the following is NOT an inherent limitation of an internal control system?

A. Management override of controls

B. Human error due to carelessness or distraction

C. Collusion between employees and outsiders

D. Automatic detection of all frauds (2 marks)

8. Control risk should be assessed in terms of .

A. special controls

B. types of potential fraud

C. financial statement assertions

D. control environment factors (2 marks)

9. Data mining is a set of computer-assisted techniques that use .

A. unusual transactions

B. sophisticated statistical data

C. databases such as ABI

D. investigative data (2 marks)

10. The Companies Act requires that directors’ reports to shareholders should take the form of .

A. bank reconciliations

B. annual accounts

C. tax assessment returns

D. audit working papers (2 marks)

11. Concealment of theft in stock records is often achieved by .

A. writing off stock as obsolete

B. failing to bank cheques promptly

C. inflating payroll figures

D. misstating investment income (2 marks)

12. Which one of the following documents is kept in the permanent audit file?

A. Management letter for the current year

B. Current year’s bank reconciliation

C. Articles of Association

D. Audit program for the year (2 marks)

13. A retiring auditor may remain in office without a resolution being passed, EXCEPT where .

A. he was appointed by the directors at the commencement of the company business to stay in office until the end of the first Annual General Meeting (AGM) where shareholders appoint an auditor

B. he is not qualified for re-appointment

C. a resolution is passed at the AGM appointing another person in his place or providing expressly that he shall not be re-appointed

D. he has given notice in writing of his unwillingness to be re-appointed (2 marks)

14. In regulating the activities of auditors, the Institute of Certified Public Accountants of Kenya (ICPAK), makes the following provisions, EXCEPT .

A. only practicing members may conduct audits

B. to be licensed to practice, a member of ICPAK must have attained more than two years’ experience in independent audit work

C. to be licensed to practice, a member of ICPAK must be a holder of a bachelor’s degree in addition to qualifying in CPA examinations conducted by KASNEB

D. to practice, members must bear a practicing license renewed every year by ICPAK (2 marks)

15. Which one of the following matters might the auditor need to consider when gaining an understanding of the specific business operation of an audit client?

A. Leasing of property plant and equipment for use in the client business

B. Products, services and market of client business

C. Acquisition or disposal of client business activities

D. Accounting policies and industry specific practice relevant to client business (2 marks)

16. Understatement is a key audit risk associated with trade payables. Which one of the following procedures might provide the MOST reliable evidence of the completeness of amount due?

A. Reconciliation of year-end supplier statement

B. Tracing of amounts due per the payable ledger to purchase invoice

C. Matching of purchase invoice to goods received notes

D. Reconciliation of the payable ledger with purchase invoice (2 marks)

17. All work done by the external auditors should be documented in their working papers regardless of whether it relates to an interim or a final audit. The following are reasons for preparing audit documentation, EXCEPT they

.

A. provide evidence for basis of key conclusions

B. enable senior team members to direct, supervise and review the audit work

C. ensure that the auditors cannot be sued for negligence

D. enable quality control review to be performed (2 marks)

18. Written representation is obtained by the auditor from management to support other evidence. Which of the following matters would a written representation NOT be suitable as audit evidence?

A. That subsequent events requiring adjustment or disclosure in the financial statement have been dealt with appropriately

B. That the payroll charge for three months of the year when the accounting records are unavailable is correctly stated

C. That management has fulfilled their responsibility for preparation and presentation of the financial statement

D. That all deficiencies in the internal controls known to management have been communicated to the auditors (2 marks)

19. Independence of the auditor may suffer a self-interest threat, when the audit fees from one client represent a large proportion of the total fee’s income of the audit firm.

With reference to the following statements, choose the CORRECT answer for an audit client that is a public interest entity?

A. If fees from the client exceeds 15% for more than a year, a safeguard must be applied to reduce the threat to an acceptable level

B. If fees from the client exceeds 15% for more than two years, the audit firm must resign from the assignment

C. If fees from the client exceeds 15% for two consecutive years a safeguard must be applied to reduce the threat to an acceptable level

D. If fees from the client exceeds 15% for any year, no safeguards are necessary as long as that fact has been disclosed to those charged with governance (2 marks)

20. Which one of the following is NOT a recognised threat to independence and objectivity as identified by the auditors professional code of conduct?

A. Familiarity

B. Self-review

C. Advocacy

D. Integrity (2 marks)

21. The following are uses of test data for test of controls in Computer Assisted Audit Techniques (CAATs) , EXCEPT .

A. used to check the controls that prevent the processing of invalid data

B. used to test processing in an integrated test facility (dummy unit)

C. used to test the controls and correct the results of processing if they differ from expectation of the auditor

D. used to test specific controls in computer programs, for example, online passwords and data access control (2 marks)

22. On 1 January 2025, Amani Ltd.’s warehouse was destroyed by fire. How should this be treated in the financial statements for the year ended 31 December 2025?

A. Only explain the event in notes to financial statements

B. No adjustment or disclosure is required

C. Adjust the financial statements to write off the warehouse and explain the event in a note to the financial statements

D. Only adjust the financial statement to write off the warehouse (2 marks)

23. “An engagement quality control review” is defined as .

A. an evaluation of the operating effectiveness of the entity’s controls

B. a review of the work of less experienced team members by the more experienced team members

C. a review to ensure that the entity is a going concern

D. an objective evaluation of the significant judgments made by the engagement team (2 marks)

24. When issuing unqualified opinion, the auditor who evaluates the audit findings should be satisfied that

.

A. estimates of the total likely misstatements is less than materiality level

B. estimates of the total likely misstatements is more than materiality level

C. estimates of the total misstatements cannot be made

D. amount of known misstatements is documented in the working papers (2 marks)

25. Which one of the following statements about the reliability of written representation is MOST accurate?

A. Written representations are sufficient and appropriate audit evidence on their own

B. Written representations are the primary source of audit evidence

C. Written representations should be used in conjunction with other audit procedures

D. Written representations are only needed for large complex organisations (2 marks)

26. What is the current auditor’s report likely to be in a scenario where the previous periods financial statements are unaudited and sufficient appropriate audit evidence is unavailable?

A. Qualified on the basis of scope limitation

B. Unqualified on the basis that the comparatives are unaudited and no opinion is expressed on them

C. Qualified on the basis that the comparatives are unaudited and an opinion is expressed on them

D. Qualified on the basis that the comparatives are unaudited and no opinion is expressed on them (2 marks)

27. Which one of the following audits is conducted between two annual audits?

A. Internal audit

B. Interim audit

C. Final audit

D. Continuous audit (2 marks)

28. While vouching for wages, an auditor should examine whether there is proper segregation of duties. Which one of the following activities should NOT be done by the same department?

A. Maintaining personnel records and approving changes in wages rates

B. Preparing pay roll summary and disbursement of wages

C. Making salary statements and filing tax returns

D. Comparing time clock records with time reports prepared by supervisors and preparing list of workers employed along with the units of production for each one of them (2 marks)

29. When performing an audit of a not-for-profit organisation, which one of the following would be a KEY audit consideration?

A. The company’s ability to generate consistent revenue

B. The proper recording of donations and grants

C. The financial impact of stockholder dividends

D. The complexity of financial instruments used (2 marks)

30. An auditor has assessed the risk of material misstatement as high. What does this imply for the audit strategy?

A. Less detailed testing will be required

B. More substantive testing should be performed

C. Less audit evidence is needed

D. The auditor could rely more on internal controls (2 marks)

31. The auditor must assess the likelihood of material misstatement in the financial statements based on .

A. the company’s internal control system

B. the information obtained through client discussions

C. the overall risk of fraud and error

D. both inherent and control risks (2 marks)

32. What is#8220;audit sampling”?

A. The process of testing a small subset of items in a population to draw conclusions about the entire population

B. The process of analysing every transaction in the financial statements

C. The process of confirming balances with third parties

D. The process of reviewing transactions for compliance with tax regulations (2 marks)

33. An auditor is responsible for detecting material misstatements in the financial statements. Which one of the following factors influences the detection risk?

A. The nature of the financial statements

B. The auditor’s use of substantive procedures

C. The auditor’s independence

D. The effectiveness of the client’s internal controls (2 marks)

34. Which one of the following statements is a limitation of using audit sampling?

A. It provides evidence about the entire population

B. It is more efficient than testing every item in the population

C. It may not detect all misstatements in the population

D. It guarantees the detection of all material misstatements (2 marks)

35. Which one of the following statements represents the BEST form of evidence for testing the accuracy of revenue recognition?

A. Reviewing the company’s revenue policies

B. Sending confirmation requests to customers

C. Analysing the company’s sales budget

D. Observing the company’s sales meetings (2 marks)

36. Which of the following procedures is MOST likely to detect unrecorded liabilities?

A. Reviewing the client’s general ledger

B. Performing cutoff tests at year-end

C. Reviewing the client’s cash receipts

D. Sending confirmation requests to suppliers (2 marks)

37. Which one of the following stages of an audit would analytical procedures NOT be used?

A. Substantive procedures

B. Planning the audit

C. Test of controls

D. Overall review (2 marks)

38. The professional code of ethics and conduct for accountants establishes a conceptual framework approach to independence.

(i) Safeguards must be applied to all threats identified

(ii) The auditors should resign from the audit engagement if the threats are significant

(iii) The conceptual framework must be applied to identify threats to compliance with the fundamental principles

(iv) Threats must be eliminated or reduced to an acceptable level

Which of the following statements are TRUE?

A. (i) and (ii)

B. (ii) and (iii)

C. (iii) and (iv)

D. (ii) and (iv) (2 marks)

39. LC’s auditors found unexpectedly high deviation rate in carrying out test of control on a sample of sales invoices. They are considering the following set of actions:

(i) Extend the sample size

(ii) Replace sample

(iii) Perform alternative substantive procedures

Which one of the following are proper actions to take?

A. (i) and (ii) only

B. (i) and (iii) only

C. (ii) and (iii) only

D. (i), (ii) and (iii) (2 marks)

40. Which one of the following audit procedures would provide the auditor with evidence that the inventory count has been completed?

A. Tracing test counts performed at inventory count to detect inventory count

B. Reviewing the physical condition of inventory during the inventory count

C. Casting (recalculating) the inventory listing

D. Vouching the cost of sample inventory items to suppliers’ invoices (2 marks)

41. When relying on the work of internal auditors, external auditors should .

A. assume full responsibility without further testing

B. evaluate the competence and objectivity of the internal auditors

C. request management to explain the internal audit findings

D. issue a disclaimer of opinion (2 marks)

42. Which one of the following statements BEST describes the principle of objectivity in auditing?

A. Using sampling techniques during substantive testing

B. Exercising unbiased judgment and avoiding conflicts of interest

C. Disclosing confidential client information when required

D. Relying on internal auditors to reduce workload (2 marks)

43. Written representations are used by the auditor to .

A. replace substantive testing

B. confirm management’s oral statements

C. guarantee internal control effectiveness

D. provide legal advice (2 marks)

44. Which one of the following controls reduces the risk of fictitious sales?

A. Regular stocktaking

B. Independent review of customer orders

C. Monthly payroll reconciliation

D. Inventory valuation reviews (2 marks)

45. Which one of the following statements is TRUE in relation to the final audit of financial statements?

A. It is ideal for large entities with voluminous transactions

B. It is a complete audit with the opinion of the auditor’s report on whether the financial statements give the true and fair view

C. It is necessary where a company is contemplating a merger or takeover bid

D. It seeks to identify outdated procedures which needs replacement and therefore the auditor provides a recommendation for their replacement (2 marks)

46. During an audit team meeting, the supervisor outlined the contents of the audit program for discussion in the meeting. Which one of the following items is NOT contained in an audit program?

A. A summary of the resources required

B. The audit objectives for each area being audited

C. The audit procedures to be carried out in meeting the objectives

D. A time budget in which hours are budgeted for various audit areas or procedures (2 marks)

47. Which one of the following is NOT a benefit of Computer Assisted Audit Techniques (CAATs)?

A. They integrate with commonly used data storage platforms

B. They are user friendly and can be operated with ease by most auditors

C. They are very expensive and therefore only for the largest companies

D. They come prebuilt with many common analyses and report available (2 marks)

48. Fraudulent financial reporting involves intentional misstatement or omissions of amounts or disclosure in the financial statements to deceive financial statement users. Fraudulent financial reporting is LEAST likely to involve .

A. deception such as manipulation, falsification, or alteration of accounting records or supporting documents from which the financial statements are prepared

B. misrepresentation in, or intentional omission from the financial statements of events, transactions or other significant information

C. intentional misapplication of accounting principles relating to measurements, recognition, classification, presentation or disclosure

D. embezzling receipts, stealing physical or intangible assets or causing an entity to pay for goods and services not received (2 marks)

49. When issuing unqualified opinion, the auditor who evaluates the audit findings should be satisfied that the

.

A. amount of known misstatements is documented in working papers

B. estimates of the total likely misstatements is less than materiality level

C. estimate of total likely misstatement is more that materiality level

D. estimate of the total likely misstatement cannot be made (2 marks)

50. In which of the following situations MUST the auditor deliver a written statement of circumstances?

(i) If the auditor is removed from office

(ii) If the auditor resigns before expiry of their term of office

(iii) If the auditor proposes to issue a modified audit report

(iv) If the auditor does not seek reappointment at the next annual general meeting for any reason

A. (i) and (ii) only

B. (i), (ii) and (iv)

C. (ii), (iii) and (iv)

D. (ii) and (iii) only (2 marks)

……………………………………………………………………………