Original price was: KSh600.KSh499Current price is: KSh499.

Download April 2025 Advanced Financial Management Answers in Pdf form

Description

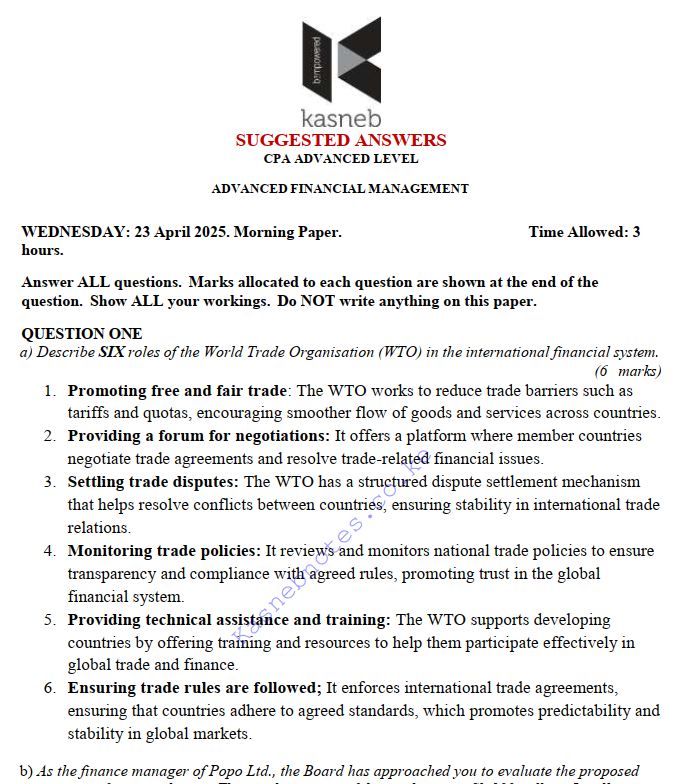

CPA ADVANCED LEVEL ADVANCED FINANCIAL MANAGEMENT

WEDNESDAY: 23 April 2025. Morning Paper. Time Allowed: 3 hours.

Answer ALL questions. Marks allocated to each question are shown at the end of the question. Show ALL your workings. Do NOT write anything on this paper.

QUESTION ONE

(a) Describe SIX roles of the World Trade Organisation (WTO) in the international financial system. (6 marks)

(b) As the finance manager of Popo Ltd., the Board has approached you to evaluate the proposed acquisition of new machinery. The purchase price of the machinery is Sh.100 million. It will cost another Sh.20 million to modify it for special use. The machine will be sold after 5 years for Sh.40 million and it will require an increase in net operating working capital (NOWC) of Sh.8 million.

Additional information:

1. The purchase of the new machine will not have any effect on revenues but it is expected to save the company Sh.45 million per year before tax operating costs mainly labour.

2. The corporate tax rate is 30%.

3. The company uses the straight line method of depreciation.

4. The project cost of capital is 12%.

Required:

(i) Using the net present value (NPV) method, evaluate whether the machinery should be purchased.

(5 marks)

(ii) Assume the Board suggests that you conduct a scenario analysis for this project because of the uncertainties of cost savings, salvage value and net operating working capital. After an extensive analysis, you come up with the following probabilities and the values for the scenario analysis:

Scenario Probability Before tax

savings Salvage value Net operating working

capital (NOWC)

Sh.“million” Sh.“million” Sh.“million”

Worst case 0.30 36 32 6.4

Base case 0.40 45 40 8.0

Best case 0.30 54 48 9.6

Required:

The project’s expected net present values (ENPV). (6 marks)

(iii) Analyse THREE common pitfalls that could arise in estimating cash flows in capital budgeting.

(3 marks)

(Total: 20 marks)

QUESTION TWO

(a) Discuss the following theories of capital structure:

(i) Pecking order theory. (2 marks)

(ii) Static trade off theory. (2 marks)

(iii) Agency effect theory. (2 marks)

(b) A financial manager has the following bond portfolio:

Bond Price (Sh.) Yield (%) Par amount owed (Sh.“million”) Duration

A 120 10 4 3.86

B 85.50 10 5 8.05

C 130.50 10 3 9.17

The three bonds are option-free.

Required:

(i) The bond portfolio duration. (6 marks)

(ii) Interpret the result obtained in (b) (i) above. (1 mark)

(c) Solomon Wasike took a mortgage product to acquire a family house with the following characteristics:

1. Mortgage loan amount was Sh.10,000,000.

2. Annual interest rate is at 8% per annum.

3. The loan is for a one year term.

4. Solomon pays an extra Sh.200,000 per month.

Required:

(i) Calculate the monthly payment for a fixed mortgage of this type. (2 marks)

(ii) Prepare the mortgage amortisation schedule for Solomon Wasike. (5 marks)

(Total: 20 marks)

QUESTION THREE

(a) Explain FOUR advantages of over-the-counter agreements in relation to the operations of the derivatives markets. (4 marks)

(b) In relation to corporate reorganisation and restructuring, examine SIX financial restructuring strategies available to a firm. (6 marks)

(c) Huge Ltd. is considering acquisition of Tiny Ltd. through a share exchange arrangement. Under the terms of acquisition, Huge Ltd. will offer two of its ordinary shares in exchange for every three ordinary shares in Tiny Ltd.

The summarised financial information relating to the two companies for the year ended 31 December 2024 are as shown below:

Huge Ltd. Tiny Ltd.

Profit after tax (Sh.) 225 million 45 million

Number of ordinary shares 37.5 million 12 million

Earnings per share (Sh.) 7.20 4.50

Market price per share (Sh.) 93.60 40.50

Price earnings (P/E) ratio 13 times 9.00 times

Required:

(i) The earnings per share (EPS) of the combined company after acquisition. (3 marks)

(ii) Assume the price earnings ratio after acquisition falls to 12 times, determine the premium received by the shareholders of Tiny Ltd. (Use the combined company’s new share price). (3 marks)

(iii) Assume that the price earnings (P/E) ratio after acquisition falls to 12 times, justify whether acquisition would be beneficial to the shareholders of Huge Ltd. (4 marks) (Total: 20 marks)

QUESTION FOUR

(a) Explain FOUR differences between “portfolio theory” and “arbitrage pricing theory”. (4 marks)

(b) The table below gives the end of year levels of the price of an ordinary share in Tausi Ltd. and a representative stock exchange index:

Year Tausi Ltd. share price (Sh.) Stock Exchange Index

2019 75 752

2020 78 815.5

2021 81 875

2022 79 840

2023 85 900

2024 76.5 795

Additional information:

1. The risk free rate is 5% per year.

2. The expected return from equities is 8% per year.

Required:

(i) The beta coefficient of Tausi Ltd.’s ordinary shares. (6 marks)

(ii) The required rate of return of Tausi Ltd.’s ordinary shares. (2 marks)

(iii) Assume that the expected rate of return of Tausi Ltd. is 10%. Establish whether Tausi Ltd. share is undervalued or overvalued. (2 marks)

(c) Hakika business solutions is a newly established firm based in Kenya and is a subsidiary of United Kingdom (UK) based company, Quick Solutions Ltd. The foreign country is Kenya while the home country is United Kingdom (UK). The projected cash flows in Ksh. from 2025 to 2029 are shown below:

Year 2025 2026 2027 2028 2029

KSh. “000” KSh. “000” KSh. “000” KSh. “000” KSh. “000”

Cash inflows 2,000 2,200 2,420 2,662 2,928

Less: Variable cash outflows (600) (660) (726) (799) (878)

Less: Fixed cash outflows (200) (200) (200) (200) (200)

Less: Depreciation (1,000) (1,000) 1,000 1,000 1,000

Cash flows before corporate tax 200 340 494 663 850

Less: 33% corporate tax (66) (112) (163) (219) (280)

Add: Depreciation 1,000 1,000 1,000 1,000 1,000

After tax corporate tax flows 1,134 1,228 1,331 1,444 1,569

Less: 10% withholding tax on dividend (113) (123) (133) (144) (157)

Net cash to be repatriated 1,021 1,105 1,198 1,300 1,412

Additional information:

1. The exchange rate of KSh/GBP is KSh 170 to 1GBP.

2. The difference in the interest rates between Kenya shillings (KSh) and Great Britain Pound (GBP) is provided by the following formula:

t

Ft = S0 × 1+rd

1+rf

Where:

Ft is the forward exchange rate at time “t”

So is the spot exchange rate

rd is the nominal interest rate in domestic currency rf is the nominal interest rate in foreign currency

3. The expected interest rates for Kenya and United Kingdom are given as 6% and 4% respectively.

4. Quick Solutions Ltd. spent Ksh 6 billion to set up the business in Kenya. A UK business conglomerate has agreed to buy the business for Ksh.10 billion in 5 years.

5. The UK cost of capital is 15%.

Required:

Compute the Net Present Value (NPV) of the project using home currency approach and comment on your findings. (6 marks)

(Total: 20 marks)

QUESTION FIVE

(a) Jawabu Ltd. is a 100% equity financed company. The company is considering undertaking a major diversification in the consumer electronics industry. Its current equity Beta is 1.2, while the average equity Beta (β) of electronics industry is 1.6.

Gearing in the electronics industry averages 30% debt and 70% equity. Corporate debt is considered risk free.

Additional information:

1. Expected return on the market is 25%.

2. The risk-free rate of return is 10%.

3. The corporation tax rate is 30% per annum.

Required:

Using suitable discount rate for the new investment, determine the weighted average cost of capital (WACC) assuming Jawabu Ltd. were to be financed in each of the following ways:

(i) 20% debt and 80% equity. (3 marks)

(ii) 30% debt and 70% equity. (3 marks)

(b) Viruga Ltd. is an unlevered firm. The firm expects to generate earnings before interest and tax (EBIT) of Sh.20 million each year in perpetuity. The firm’s current market value is Sh.120 million and pays corporation tax at the rate of 30%. The management of the firm is considering the use of debt financing. The firm’s financial analyst has estimated that the present value of any future financial distress cost is Sh.80 million and that the probability of financial distress would increase with leverage according to the following schedule:

Value of debt

Sh.“million” Probability of financial distress Pre-tax cost of debt (%)

25 0.000 7

50 0.0125 8

75 0.0250 9

100 0.0625 10

125 0.1250 11

150 0.3125 12

200 0.750 13

Required:

(i) The current cost of equity and weighted average cost of capital (WACC) of the firm. (2 marks)

(ii) The firm’s optimal level of debt financing using the “Pure” Modigliani and Miller with corporate tax model. (6 marks)

(iii) The firm’s optimal level of debt financing using Modigliani and Miller with corporate taxes and financial distress. (6 marks)

(Total: 20 marks)

………………………………………………………………………..

Related products

-

August 2024 CPA Auditing and Assurance Past Paper answers

Original price was: KSh300.KSh199Current price is: KSh199. Download -

August 2024 CPA Advanced Financial Reporting and Analysis Answers

Original price was: KSh300.KSh199Current price is: KSh199. Download -

- CPA Advanced Financial Management (AFM) Year 2015 to 2019 Answers

Original price was: KSh999.KSh699Current price is: KSh699. Download -

Advanced Financial Management November 2016 Past Paper and Answers

Original price was: KSh399.KSh199Current price is: KSh199. Download