Original price was: KSh300.KSh199Current price is: KSh199.

Download August 2024 CPA Advanced Auditing and Assurance Past papers with answers in Pdf form

Description

DOWNLOAD ANSWERS TO THESE QUESTIONS

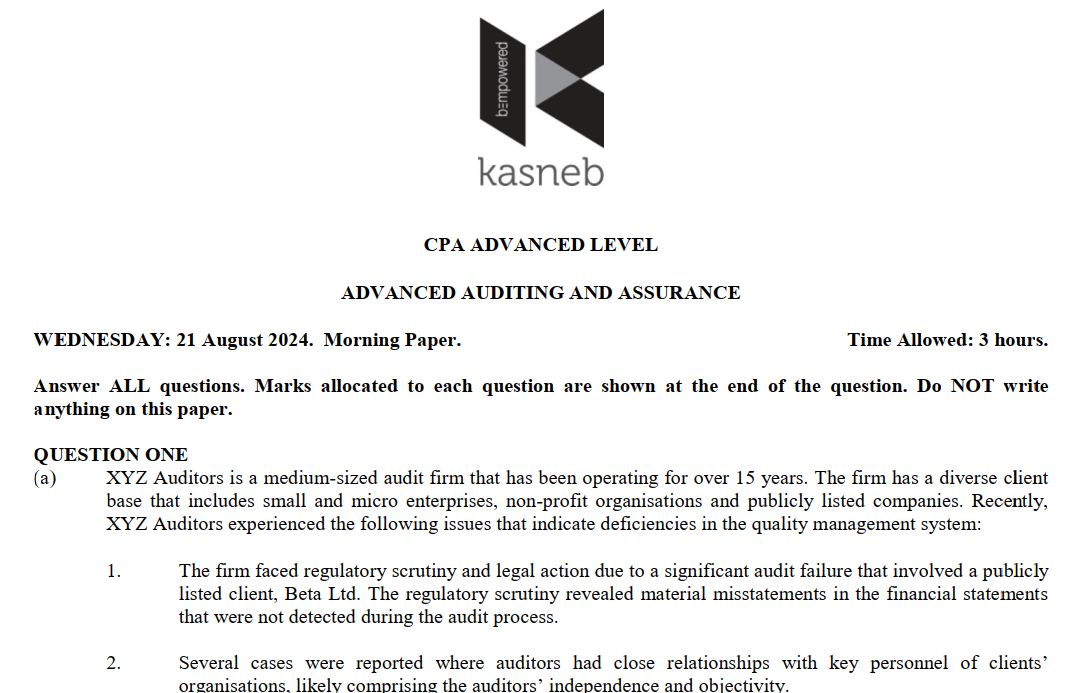

CPA ADVANCED LEVEL ADVANCED AUDITING AND ASSURANCE

WEDNESDAY: 21 August 2024. Morning Paper. Time Allowed: 3 hours.

Answer ALL questions. Marks allocated to each question are shown at the end of the question. Do NOT write anything on this paper.

QUESTION ONE

(a) XYZ Auditors is a medium-sized audit firm that has been operating for over 15 years. The firm has a diverse client base that includes small and micro enterprises, non-profit organisations and publicly listed companies. Recently, XYZ Auditors experienced the following issues that indicate deficiencies in the quality management system:

1. The firm faced regulatory scrutiny and legal action due to a significant audit failure that involved a publicly listed client, Beta Ltd. The regulatory scrutiny revealed material misstatements in the financial statements that were not detected during the audit process.

2. Several cases were reported where auditors had close relationships with key personnel of clients’ organisations, likely comprising the auditors’ independence and objectivity.

3. Meanwhile, many audit staff had not received sufficient training on recent changes in auditing standards and new regulatory requirements.

4. The firm often struggled with resource allocation, resulting to audit staff being overburdened and rushed audits, which led to the quality of audits being compromised.

5. Inconsistencies in audit documentation coupled with lack of sufficient audit evidence to support conclusions reached in several audit engagements was also noted.

The above issues have prompted the firm’s top management to consider implementing International Standard on Quality Management 1(ISQM1) to enhance their quality management system and address these deficiencies.

Required:

Analyse SIX components of ISQM1 that XYZ Auditors should focus on to address the issues raised to comply with the standard. (6 marks)

(b) International Standard on Auditing (ISA) 520, “Analytical Procedures”, requires auditors to perform analytical procedures at various stages of audit risk assessment.

Required:

(i) Explain FIVE objectives of performing analytical procedures as part of audit risk assessment. (5 marks)

(ii) Highlight THREE limitations of performing analytical procedures at the planning stage of the final audit.

(3 marks)

(c) You are a senior auditor in the audit of Bayeti Ltd., a medium-sized company which sells a limited range of industrial products. While performing reviews on Bayeti Ltd.’s audit files, you have noted that a number of creditors have withdrawn their financial support to your client and that your client has defaulted on a number of loans. The working papers conclude that the going concern assumption is inappropriate and recommends that a note explaining the cash flow challenges your client is facing be included in the financial statements. However, the directors are reluctant to include the note in the financial statements.

Required:

In each case, discuss THREE implications on the audit report if:

(i) The directors refuse to disclose the note. (3 marks)

(ii) The directors agree to disclose the note. (3 marks)

(Total: 20 marks)

QUESTION TWO

(a) Tech Innovators Ltd. is a 2-year-old startup seeking to attract significant venture capital investment. Your firm has been appointed by Tech Innovators Ltd. to conduct a due diligence investigation. You are the partner responsible for the audit of Tech Innovators Ltd. The due diligence process involves reviewing the prospective financial information provided by the client and also a social and environmental audit to assess the company’s compliance with sustainability practices.

Required:

(i) Describe FIVE areas of interest you could consider in evaluating the prospective financial information relevant while conducting the due diligence process. (5 marks)

(ii) Analyse FIVE factors you might consider while undertaking the social and environmental audit. (5 marks)

(b) You are the Audit Manager of Maharabu and Maharabu Associates, a firm of Certified Public Accountants, responsible for the audit of Madeni Ltd. You are currently reviewing the working papers of the audit for the year ended 31 December 2023. While reviewing the working papers on the payroll with the audit junior, he mentioned the following:

“A number of new employees were hired during the year, with Sh.1.35 million being paid to them. No documentation is available to show that the board had authorised the hiring of additional members of staff. When I questioned the payroll supervisor, she mentioned that she made the additions. She said that no authorisation was required from the board, because the new employees were hired on a temporary basis. Conversely, when making enquiries about the staffing levels from the management, it was stated that no new employees had been taken on board for the year under review”.

Other than the tests of controls planned, no other audit work has been performed.

Required:

(i) Explain the meaning of the term#8220;professional skepticism”. (2 marks)

(ii) In relation to the audit of Madeni Ltd.’s payroll, recommend FOUR actions that should be taken by the auditor. (8 marks)

(Total: 20 marks)

QUESTION THREE

(a) You are the Audit Manager of Mateo and Associates, a firm of Certified Public Accountants who are the auditors of Miradi Group of Companies Ltd. for the year ended 31 December 2023. Miradi Group of Companies Ltd. is a financial services company. The group has three subsidiaries namely; Kasi Ltd. which provides capital markets services, Taurus Ltd. which provides brokerage, investment and wealth management services and Gold Crowns Ltd. which undertakes asset management and other related services. The year-end is almost complete and the following matters have been raised by the audit senior for your attention:

1. Kasi Ltd. is experiencing going concern problems as noted during this year’s audit. Unless it secures the prospected loan from the bank to finance a contract already won, Kasi Ltd. will be unable to continue in operation in the foreseeable future. No disclosure of the going concern problems have been made.

The audit senior has suggested that, due to the seriousness of the situation, the audit opinion should be qualified ‘except for’.

2. Taurus Ltd. has changed its accounting policy on buildings from cost model to revaluation model. No disclosure of this change has been given in the financial statements. The carrying amount of the premises in the statement of financial position as at 31 December 2023 is the same as at 31 December 2022. The buildings figure is material in the context of the financial statements. The audit senior is satisfied with the carrying value of the buildings in the statement of financial position.

The audit senior has concluded that a qualification is not required but suggests that attention can be drawn to the change in accounting policy by way of an emphasis of matter paragraph.

3. The directors’ report of Gold Crowns Ltd. states that the company’s revenues have grown from 1.2 % to 4% in the last one year. However, analytical review procedures revealed that revenues had only grown by

1.65 %. The audit senior is satisfied that the revenue figures are correct.

The audit senior has noted that an unmodified opinion should be given as the audit opinion does not extend to the directors’ report.

Required:

For each case mentioned above:

(i) Comment on the appropriateness or otherwise of the audit senior’s proposals regarding the auditors’ reports. (3 marks)

(ii) Where you disagree, indicate what audit modification (if any) should be given instead. (6 marks)

(b) You are the audit engagement partner in the audit of Alina Ltd. An audit trainee assigned to you is considering ending his internship programme after he learnt that auditors are potentially liable for both criminal and civil offences in the conduct of an audit.

Required:

(i) Citing relevant examples in each case, distinguish between auditors “criminal liability” and “civil liability”.

(6 marks)

(ii) Highlight FOUR conditions that the company must prove under criminal liability in order to succeed against the auditor in damages. (5 marks)

(Total: 20 marks)

QUESTION FOUR

(a) Auditor independence is part of the foundation of the auditing profession. An independent, reliable and ethically sound audit gives a company credibility and allows the public to trust in the accuracy of the results and the integrity of the accounting profession.

With reference to the Institute of Certified Public Accountants of Kenya (ICPAK) ethical guidelines, justify FIVE

reasons why professional independence is considered important to the auditor. (5 marks)

(b) You are a senior auditor in the audit of Jasiri Ltd., a medium sized manufacturing company. The audit of the financial statements for the year ended 30 June 2024 is almost complete and you are reviewing the audit files for the period. The following issues have prompted the senior auditor to call for a meeting with the client’s top management to be held in a weeks’ time:

1. There were questions concerning the accuracy of the depreciation charged in the financial statements and a preliminary investigation revealed that the computerised accounting system had failed to compute depreciation of equipment correctly resulting to an overstatement of the depreciation value by Sh.780,975. The book value of the equipment had been overstated by Sh.1,128,340. The equipment value for the year ended 30 June 2024 was Sh.7,135,725.

2. At the beginning of the year 2024, the company had issued a loan to Sarah Hagoi, one of the members of the top management, amounting to Sh.500,000. On further examination of the records, it was discovered that the loan had not been disclosed in the financial statements because it was considered immaterial.

3. During the year ended 30 June 2024, the company made a reduction on its provision for customer warranties recognised in the financial statements. During the past two years, the provision has been made at the rate of 10% of sales for three months. The management has however decided to reduce it to 5% on the claims that the quality assurance processes had improved and therefore customer warranty claims were likely to reduce. Further investigations however revealed that warranty claims have by far remained the same as in previous periods.

Required:

(i) Discuss how the auditor would be expected to treat each scenario mentioned above for the purpose of reporting. (9 marks)

(ii) Propose how you would treat each scenario mentioned above in the auditors report assuming the management of Jasiri Ltd. does not correct the misstatements. (6 marks) (Total: 20 marks)

QUESTION FIVE

(a) Discuss the audit supervisor’s responsibilities in relation to supervision of the audit assistants work during the audit of financial statements. (4 marks)

(b) In the context of audit assurance engagements, describe how “attestation engagements” differ from “direct reporting engagements”. (4 marks)

(c) Artificial intelligence (AI) is often described as ‘an evolving technology’ that is equipping computer systems with something akin to human intelligence.

Required:

With reference to the above statement, argue TWO cases for and TWO cases against the use of artificial intelligence in the audit practice. (4 marks)

(d) Evaluate FOUR differences between “forensic audit” and “historical audit” of financial statements. (8 marks)

(Total: 20 marks)

……………………………………………………………………….

Related products

-

- Collection of CPA Financial Management Past Paper Answers(September 2015 upto APRIL 2025)

Original price was: KSh899.KSh699Current price is: KSh699. Download -

Advanced Financial Management November 2016 Past Paper and Answers

Original price was: KSh399.KSh199Current price is: KSh199. Download -

August 2024 CPA Advanced Management Accounting Answers

Original price was: KSh300.KSh199Current price is: KSh199. Download -

Advanced Financial Management November 2018 Past Paper and Answers

Original price was: KSh399.KSh199Current price is: KSh199. Download