Original price was: KSh300.KSh199Current price is: KSh199.

Download April 2025 Governance and Compliance Audit Past Paper answers in Pdf form

Description

QUESTION ONE

MEGAPLAST INDUSTRIES LIMITED (MPIL)

MegaPlast Industries Limited (MPIL) is a medium-sized plastic manufacturing company based in Nairobi City County, specialising in the production of plastic packaging materials for various industries. As a key player in the sector, MPIL is subject to rigorous governance and compliance requirements, particularly concerning workplace safety, environmental sustainability and corporate accountability.

In Kenya, the manufacturing sector is under increased scrutiny due to its pivotal role in economic growth, particularly within the framework of the Bottom-Up Economic Transformation Agenda (BETA), which prioritises Agricultural Transformation; Micro, Small and Medium Enterprise (MSME) Economy; Healthcare; Housing and Settlement and Digital Superhighway and Creative Industry. Companies operating in this sector must comply with various statutes, including the Occupational Safety and Health (OSH) Act, Environmental Management and Coordination Act (EMCA) and Companies Act, which impose strict governance and compliance responsibilities.

In 2023, MPIL conducted a governance and compliance audit following concerns about workplace safety violations and potential non-compliance with environmental regulations. The audit aimed to assess the company’s adherence to occupational health and safety laws, environmental policies and governance best practices. The findings of this audit were expected to inform corrective measures, enhance regulatory compliance and strengthen corporate governance structures within the organisation.

The governance and compliance audit at MPIL aimed not only to ensure adherence to regulatory requirements but also to identify opportunities for operational efficiency and process improvement. A preliminary risk assessment was conducted to identify high-risk areas, with key areas of focus including: Compliance with occupational safety standards, adherence to environmental regulations, particularly waste management practices and effectiveness of governance structures in decision-making processes.

An audit plan was developed, outlining the scope, timeline, resources and methodologies to be used. Stakeholders at various levels including the board of directors, senior management and shop-floor supervisors, were engaged to clarify expectations and provide input on potential areas of concern. This collaborative approach was designed to facilitate a smooth and effective audit process.

Proper documentation and communication were integral to the governance audit process. The governance auditors reviewed critical documents, including:

• Health and safety policies and incident reports.

• Environmental compliance reports and waste disposal records.

• Board meeting minutes and governance charters.

• Financial and operational reports submitted to regulators.

Regular communication was maintained throughout the governance audit. It commenced with a kick-off meeting, where objectives, timelines and stakeholder roles were outlined. Weekly progress reports were shared with the management team to ensure transparency, address emerging issues promptly and minimise disruptions to company operations. A comprehensive evidence collection process was implemented using various techniques. The governance audit team also verified compliance documentation submitted to regulatory bodies, including the National Environment Management Authority (NEMA) and the Directorate of Occupational Safety and Health Services (DOSHS). All findings were meticulously documented to ensure credibility and accuracy.

The governance audit report highlighted areas of compliance, gaps and associated risks, with key findings including:

• Workplace safety gaps#8211; Non-compliance with OSHA standards, particularly inadequate worker training and poor maintenance of fire safety equipment.

• Environmental violations#8211; Improper waste disposal and the lack of recycling initiatives.

• Weak governance oversight#8211; Minimal board involvement in operational risk management and compliance oversight.

To address these issues, the governance audit team provided actionable recommendations to the board. The governance audit team held a debrief meeting with MPIL’s board and management to discuss the findings and recommendations. This led to the development of a detailed action plan, assigning timelines and responsibilities to ensure effective implementation of corrective measures.

Required:

(a) Explain FIVE benefits that MegaPlast Industries Limited (MPIL) could derive from stakeholders’ involvement in the governance audit process. (10 marks)

(b) MPIL’s governance weaknesses played a significant role in the compliance issues identified in the audit.

Analyse FIVE best practices that MPIL should adopt to strengthen board-level governance committees for compliance and risk management. (10 marks)

(c) Describe FIVE methods used to collect audit evidence at MPIL. (10 marks)

(d) Examine FIVE challenges that MPIL might face in implementing the recommended governance reforms.

(10 marks)

(Total: 40 marks)

QUESTION TWO

(a) Governance audit evidence is essential in the audit review process for forming an audit opinion.

With reference to the above statement, explain FIVE sources of governance audit evidence. (5 marks)

(b) Analyse FIVE components of governance audit management letter. (10 marks)

(Total: 15 marks)

QUESTION THREE

(a) Highlight FIVE sources of governance audit criteria. (5 marks)

(b) Explain FIVE factors to consider before appointing a governance auditor. (5 marks)

(c) Examine FIVE enablers of an effective governance audit. (5 marks)

(Total: 15 marks)

QUESTION FOUR

(a) Explain FIVE justifications for conducting an audit follow-up in a governance audit. (5 marks)

(b) Evaluate FIVE strategies that a governance auditor could use to minimise potential liability under a governance audit. (5 marks)

(c) Examine FIVE reasons for holding an inception or entry meeting with a client in a governance audit. (5 marks)

(Total: 15 marks)

QUESTION FIVE

(a) Describe FIVE roles of a Board in implementing governance audit recommendations. (5 marks)

(b) Highlight FIVE actions that management may take on events known to management that occur after the date of the governance auditor’s report but before the date the auditor’s report is issued. (5 marks)

(c) Analyse FIVE drawbacks of carrying out peer reviews in governance audit. (5 marks)

(Total: 15 marks)

……………………………………………………………………………………………………

Related products

-

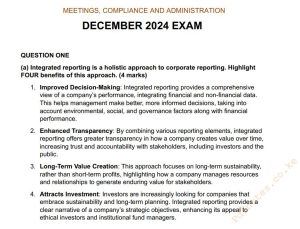

December 2024 Meetings, Compliance and Administration Past Paper Answers

Original price was: KSh300.KSh199Current price is: KSh199. Download -

August 2024 CPA CS Company Law Past Paper answers

Original price was: KSh300.KSh199Current price is: KSh199. Download -

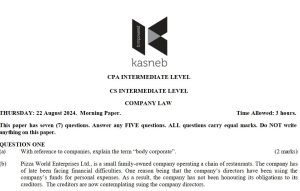

- Collection of Meetings Compliance and Administration Pdf Past Paper Answers (December 2021 to AUGUST 2025)

Original price was: KSh1,200.KSh799Current price is: KSh799. Download -

- Collection of CPA CS Information Communication Technology (ICT) Pdf Past Paper Answers (September 2015 to DECEMBER 2025)

Original price was: KSh899.KSh699Current price is: KSh699. Download